Albert, a financial service startup, raised $five million in Series A funding from investors with QED, American Express Ventures, and Portag3. This brings its overall funding to approximately $7.Five million. Read the total story right here.

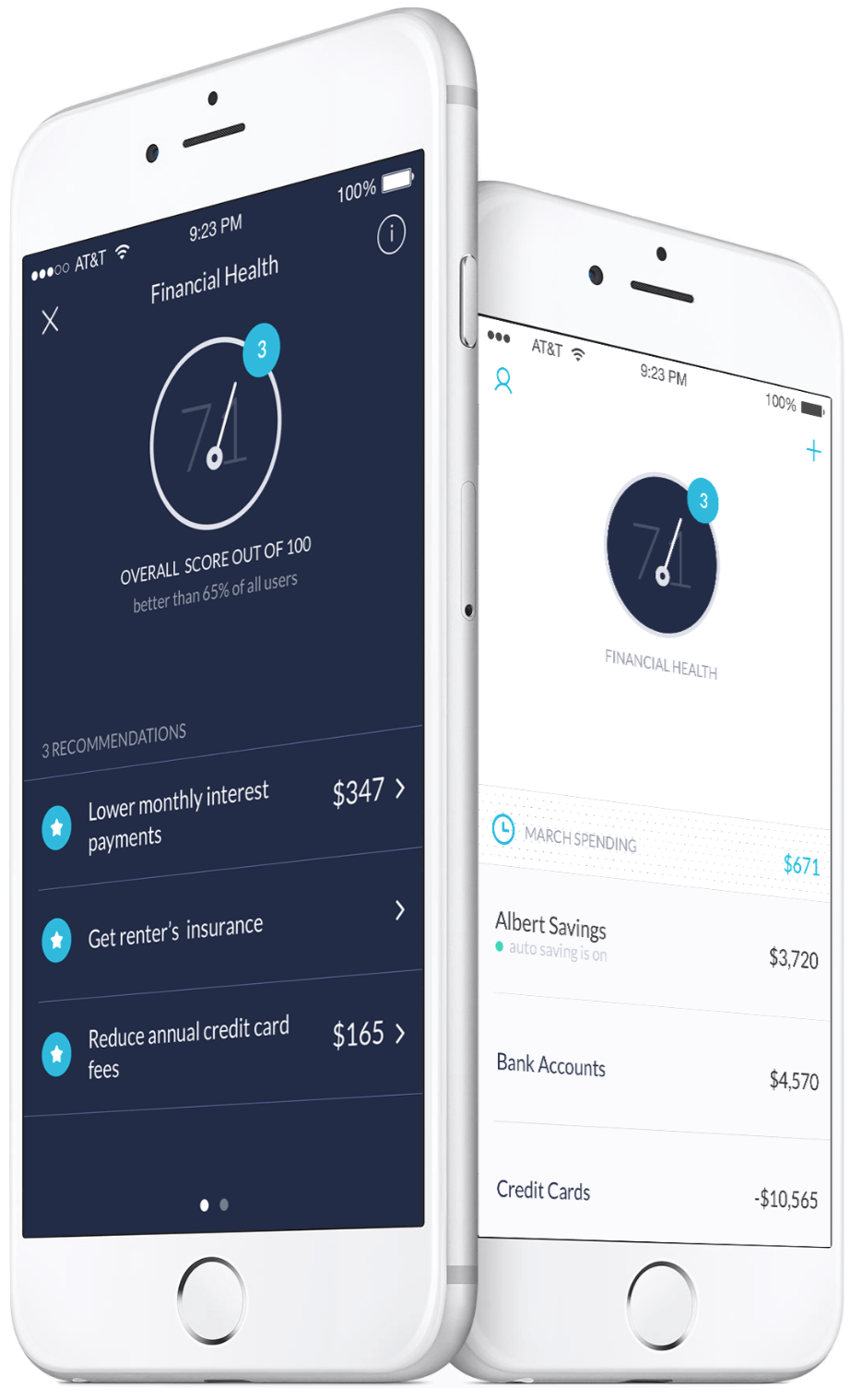

Here’s how it works: An app tracks finances and makes personalized suggestions to help customers take the movement. It’s just like different private finance apps like Mint or Digit in that it aggregates monetary information into a single portal.

It differs in that users have access to a human “monetary concierge” who doles out a customized recommendation. “People ask questions about their financial existence,” said Albert CEO Yinon Ravid. “It’s generally about paying down debt, saving extra money, or even something as easy as, ‘Where do I purchase reasonably-priced diapers?’”

This is a “pay what you need” function, in which customers pay what they think is fair based on their utilization. The minimum is $four a month.

The economic app marketplace has become saturated over a previous couple of years. My question to Ravid turned into: Can’t a competitor like Mint upload its personal team of monetary advisers, and abruptly, they have got tens of hundreds of thousands of present users geared up to open their wallets for financial advice?

“Can other human beings mirror what you’re doing in the scheme matters? Of path,” Ravid stated. “The difference is we sell customer service. We have our personal proprietary software, we’ve humans in-residence, and we’re capable of picking out things about the client in actual-time.”

The fast evolution of mobile apps in specific categories has compelled companies to begin-united the states of America to give you new ideas. Considering the simple idea of money savings, developers gambled upon the idea of an app. The app’s method might be much like that of a “money pool” and about the age-old exercise of pooling cash in small organizations of human beings. Thus, every person of the app can participate in collaborative circles of financial savings by paying a sure amount of money on a normal foundation. The stored amount may be withdrawn using the customers at times they want. This is the opportunity to credit playing cards.

However, growing an app this is efficient enough as a credit card alternative is difficult. Here is the list of effective functions that one ought to recall to create a penny saver app to allow people to keep cash with careful forethought for their short-run goals.

App ought to permit users to sign up for the saving companies.

One of the should-have features for a credit app is permitting customers from any nook of the arena to sign up in groups to shop money as consistent with their conveniences. On the pinnacle of it, it isn’t like an app where most of the customers contributing cash will win the jackpot on the stop. Its sheer idea pushes the customers to keep a few a part of the precious earnings by creating corporations. Thus, clearly, the foremost important feature of the app is to add up to users.

Flexible payment choice for users

No doubt, the success of any finance-associated app relies upon its functions to aid the users in saving up money. In this type of app, this is like a credit score card opportunity, and every other pivotal feature is its flexible charge alternatives. In this method, users have to provide a choice to pick the feed technique that they prefer. Simultaneously, the customers must be capable of using this option for paying off any quantity or invoice from the cash stored in the app while they’re in want.

Take total to manipulate of the money stored and spent.

After all, the financial institution accounts.

A credit-saving app is, in general, like a digital pocket that let users store and make bills at the cross. Henceforth, it desires to be linked to the bank bills of the users without delay. When one plans to create a money-saving, this comes as one of the indispensable features to don’t forget as customers cannot spend money on the saving account of the app until they get admission to their non-public accounts.

If you have got already a iPhone app improvement in Australia. Its handpicked team works with determination to build particular, consumer-centric, and useful apps for organizations and private services. You can visit and comply with the LinkedIn web page for modern-day tales and updates on mobile app technology.